It’s not news that electronics manufacturers are looking for ways to reduce manufacturing costs. Saving money on the purchase of capital equipment, which is a major component of overall manufacturing costs, seems like a good solution. However, selecting equipment based on the price of the equipment can be quite deceiving. The true determining factor becomes production cost per part. Also in case of dispensing equipment.

Dan Ashley, Nordson Asymtek

To make that determination, other factors come into play such as fixed costs, labor, recurring costs, yield, and the number of good parts produced. In the case of dispensing equipment, just an improvement of 0.01% yield can make a dramatic difference. Doing a complete lifetime cost of ownership analysis enables the manufacturer to evaluate the real cost of the equipment and provides a tool for seeing how to best reduce total cost of ownership.

SEMI has developed standard E35-0305 – Guide to calculate cost of ownership metrics for semiconductor manufacturing equipment (Semiconductor Equipment and Materials International, San Jose, CA, Dec. 2004). The purpose of this guide is to provide standard metrics for evaluating unit production cost effectiveness of manufacturing equipment in the semiconductor industry. This guide establishes a well-defined procedure to facilitate an understanding of equipment-related costs by providing definitions, classifications, algorithms, methods, and default values necessary to build a full or constrained cost of ownership calculator.

Cost of ownership model

We have applied SEMI’ s guidelines to dispensing equipment. The cost of ownership calculator is available under tech tools on the bottom of the page at http: //www.nordson.com/en-us/divisions/asymtek/support/Pages/Tech-Tools.aspx. Adjusting the figures and parameters in this model shows how changing just one factor can considerably increase or reduce the total cost of ownership and helps users determine what equipment characteristics are most important to reduce their production costs.

The cost of ownership (COO) equals the total cost divided by the total number of good parts. The total cost of owning the equipment consists of the sum of four major parameters:

- Initial fixed costs involved in purchasing the equipment such as purchase price, cost of installation and initial training, system qualification, and any movement of the equipment in the factory.

- Fully burdened labor cost.

- All recurring costs associated with the equipment over its lifetime. This includes such things as consumables, maintenance, utilities, floor rent, and specialized support personnel.

- The yield cost associated with the equipment’s mishandling of the devices. The cost of lost yield due to the equipment is the product of the probability that the device will be damaged by the equipment in question multiplied by the cost of the device at that processing step.

The total number of parts produced over the life of the equipment equals a formula we can refer to as L x T x Y x U. Whereas:

- L is the entire lifetime of the equipment.

- T is the throughput rate – parts or units per hour (UPH).

- Y is composite yield or the number of good units produced.

- U is equipment utilization.

Changing yield by even the smallest amount can have a major effect on cost of ownership. In dispensing equipment, many of the fea- tures that add to the cost of the equipment are the same features that contribute to improved yield, such as advancements in throughput, fluid management, and process control. Examples are automated cali- bration that shifts to pre-calibrated motor speeds between dispenses, variable valve speeds, flow rate verification, low fluid level detection, and other sophisticated software interfaces, process control, and monitoring features. Other factors, such as using non-contact jet dispensing for greater process margin, also can increase yield sig- nificantly.

Effect of initial cost of dispenser

The operating speed of the equipment (raw units per hour produced) has a near linear effect on the cost of production. Features such as using jet technology instead of needle dispensing, high speed fiducial recognition, and sophisticated software features for optimizing dispense patterns can often yield 3x to 6x improvements in throughput. This assumes that the entire production line can increase UPH by the same amount.

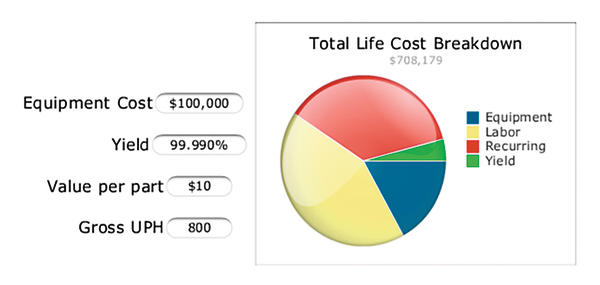

Let’s take the case of a fluid dispenser and place the initial equipment cost at 76.000 € ($ 100,000) For that price, one could obtain a dispenser with many process controls. Based on actual experience, we have data confirming a process yield of 99.99 % on that equipment and a throughput of 800 UPH. What happens, when we try to save money by purchasing a less sophisticated piece of equipment at a lower cost?

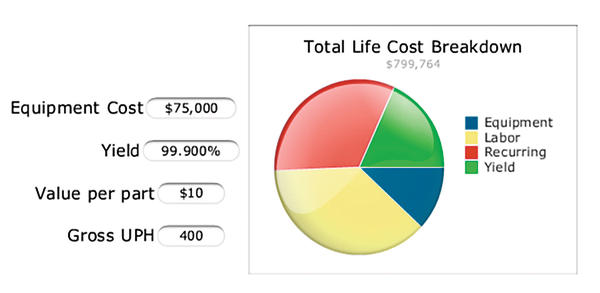

Assuming we can find a fluid dispenser that could perform similar dispensing operations to the more expensive one for a price of 57,000 € ($ 75,000) we’ve used our COO calculation tool to calculate the cost of operation. Comparing the low priced machine to the 76,000 € ($ 100,000) machine changes more variables than just the cost of the equipment. At that price, it is reasonable to assume that the equipment would lack the process control and advanced features found on the higher priced system. Therefore, speed would be slower and the yield lower. By lowering speed to say 400 UPH throughput and getting a 99.90 % yield for the lower priced equipment, the cost of ownership for the less expensive dispenser is 107 % more than the expensive one.

Besides yield and speed, other significant variables in dispensing are the costs of disposables used in the dispensing operation. What are the costs for dispensing fluid, needles, and pumps? Equipment that conserves fluid by measuring it properly and making sure it is the right temperature and viscosity so it is not wasted might be looked at as reducing COO rather than as adding to it. The same goes for other disposables required for equipment operation. Recurring costs and labor are also large percentages of the total cost of ownership. Equipment that requires less user interaction can also reduce the cost of ownership.

Conclusion

Cost of ownership is based on a multitude of variables and factors. The cost of the equipment is just one of them. Before purchasing any equipment it is wise to utilize a model such as the SEMI model we adapted for dispensing equipment. While it may require a bit more homework to apply cost of ownership analysis, it can also help drive a good decision with long term positive benefits.

SMT/Hybrid/Packaging Booth 6-430

Zusammenfassung

Es ist nicht neu, dass Elektronik-Hersteller nach Wegen suchen, um ihre Produktionskosten weiter zu senken. Eine Reduzierung der Kapitalkosten, die den höchsten Anteil an den Gesamtkosten ausmachen, ist dabei ein wichtiger Faktor. So sind die Anschaffungskosten meist entscheidend für die Auswahl des Equipments. Ein wirklich aussagefähiger Faktor sind jedoch die Produk- tionskosten pro gefertigter Baugruppe. Das gilt auch für Dispenser.

Ce n’est une nouveauté pour personne que les fabricants de composants électroniques sont en quête de solutions pour réduire leurs coûts de fabrication. Dans un tel contexte, la réduction des frais capitaux, qui constituent la majeure part des coûts totaux, est décisive. C’est la raison pour laquelle les frais d’équipements, et donc le choix de l’équipement, sont le plus souvent la cible des restrictions. Pourtant, les frais de production par composant produit sont encore plus parlants. Et cela s’applique aussi aux distributeurs.

Share:

{kind=link}