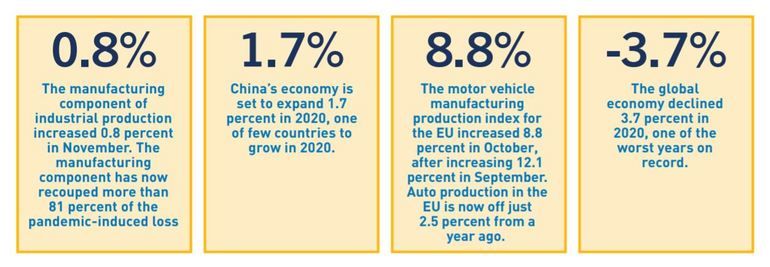

As 2020 has come to a close, the year 2021 is seen with trepidation but also with a degree of optimism. When the dust settles from the previous year, global real GDP growth will be down 3.7 percent. The United States economy has fallen by 3.5 percent during the year, the worst annual decline since the demobilization following World War II in 1946, and before that, the Great Depression. 2020 is one of the 10 worst years in the 200+ years of U.S. history.

In some ways it could have been worse. In many ways it could have been better. The decline in the second quarter left a crater like none the U.S. has experienced. The speed and depth of the decline was unheralded. This same narrative played out in most countries across the globe. But early fiscal and monetary response helped mitigate some of the potential fallout. The partial recovery in the third quarter was the strongest quarter of growth in history in the U.S., Europe and elsewhere.

Economic activity

At the same time, a resurgence of Covid-19 cases in recent months has brought renewed restrictions in the U.S. and Europe and incoming data suggests economic activity is slowing. While the damage has not been as pronounced as early in the pandemic cycle, it has curtailed growth and will prolong the recovery. In Europe, it has likely exacerbated a second decline in headline economic growth. While a double dip recession is not the base-case scenario in the U.S., the risk of a double dip recession has increased.

Nowhere is this slowdown more pronounced than with the U.S. labor market. Job growth is slowing and at the current rate, it will take until 2024 to recover all of the jobs lost to the pandemic. Temporary layoffs dropped to 2.8 million in November, but the slowdown could mean employers are turning back to furloughs as the outlook weakens. Permanent layoffs increased to 3.7 million in November and the percent of those workers who are long-term unemployed (over 27 weeks) continues to rise, leading to concerns of structural dislocations in the labor market.

The Covid-19 recession is unlike previous recessions in many ways. Typically, during a recession, consumers delay spending on durable goods while spending on services is more resilient. But in this recession, travel restrictions and mandated closures crippled the service industry. Conversely, the manufacturing industry has recovered more quickly than it might have historically as consumers reallocated spending towards the goods economy. In the U.S., spending on services is still seven percent below pre-pandemic levels, while spending on goods is now above its pre-recession peak.

Expectations for 2021

The early months of 2021 will be dictated by the trajectory of the virus. Slower growth in both the U.S. and Europe can be expected. But vaccines are now being administered to millions of people. It would take more than four years to reach herd immunity without vaccines. While the exact timing is uncertain, it appears likely that the U.S. and much of Europe can reach herd immunity with the help of vaccines by the back half of 2021. In the second half of 2021, prospects should brighten. Increased immunization should instill confidence and push economies closer to pre-pandemic normalcy. Pent-up demand should help drive economic activity.

The U.S. economy should regain its pre-pandemic levels by mid-2021, although the labor market will likely lag behind. European economies are not likely to regain their pre-pandemic levels until the end of 2022 or into 2023. This will be especially true in Southern Europe where countries are more reliant on tourism.

While the recession will likely end up being less severe than initially feared, the recovery will be long and uneven. There are also a myriad of risks that could derail the recovery like the news of a more highly contagious Covid-19 mutation. This could mean more restrictive measures in 2021 that will further hamper economic recovery. While this isn’t, as of now, the base-case scenario, it is a risk with outsized negative consequences.

Effects on manufacturing industry

The global manufacturing sector continues to recover. Many sectors have recovered from seemingly impossible collapse in the immediate aftermath of the pandemic. The auto industry in both the U.S. and Europe has recovered surprisingly well. In the U.S., the auto industry has brought back nearly 80 percent of the jobs lost this year, far better than most other sectors of the economy. Production and sales both recovered sharply, quickly making up lost ground.

The auto production in the EU is now off just 2.5 percent from a year-ago. Additional fiscal support in both the U.S. and Europe will further help mitigate some of the negative effects of the pandemic. However, the next few months will be especially vulnerable. With rapid dissemination of vaccines, growth should begin to pick up in the back half of 2021. Credit card balances are at three-year lows and savings rates are at record highs. Strong government support early in the pandemic pushed personal income up. At the same time spending was limited by the lockdown. These excess savings are now sitting on the sidelines waiting to be spent.

European economic growth

GDP for the third quarter was revised down slightly. Euro area GDP increased 12.5 percent in the third quarter (11.5 percent in the EU), the strongest quarterly growth since records began in 1995. GDP is still down 4.3 percent from 2019 (4.2 percent in the EU). France saw the strongest jump in the third quarter, rising 18.7 percent. Spain (16.7 percent increase) and Italy (15.9 percent increase) also experienced solid growth. Germany was up 8.5 percent during the quarter. Over the last month, rising Covid-19 cases have led many countries to implement lockdowns.

While not as severe as earlier in the year, the lockdowns have diminished economic activity. The lockdowns will drive GDP to contract in the final quarter of the year and lead to subdued economic activity in the first half of 2021. Further fiscal policy support, coupled with vaccine dissemination and pent-up demand, should drive growth in the back half of 2021. The economy was on track to decline just under two percent in the fourth quarter, before seeking out a small gain in the first quarter.

Employment

The unemployment rate in the EU was steady at 7.6 percent in October. In the Eurozone, the unemployment fell from 8.5 percent to 8.4 percent in October. Unemployment was 7.4 percent in the same month last year. Revisions in the last month reveal a worse unemployment rate in the aftermath of the pandemic that has slowly improved in recent months. Short-time work programs have helped to mitigate the impact of the pandemic on employment. While October brought increased Covid related restrictions, initial data suggests these measures haven’t yet materialized in higher unemployment.

Manufacturers’ sentiment (PMI)

The Eurozone’s manufacturing PMI decreased slightly in November, falling from 54.8 to 53.8, likely driven by new lockdown measures and curtailed economic activity. Despite these new restrictions, the manufacturing sector continued to expand in November and early indicators suggest the same for December. Unlike normal recessions, the manufacturing sector continues to expand following the initial punch of the pandemic while the service sector continues to languish. Europe manufacturing is being buoyed in particular by strong growth from German producers.

E.U. end markets for electronics

While renewed restrictions have reduced mobility and curtailed some spending, the industrial sector in Europe continues to recover. The manufacturing output index for the EU rose in October, increasing 1.8 percent. Output remains down 3.3 percent from last year.

Computer, electronics and optical products: The electronics industry, which includes categories such as components, loaded boards, computers, communications equipment and consumer electronics, increased three percent in October. The sector is off 12.9 percent from last year.

Motor vehicles: The Motor vehicle manufacturing production index increased 8.8 percent in October, after increasing 12.1 percent in September. Auto production in the EU is now off just 2.5 percent from a year-ago.

Air, spacecraft and related machinery: The air and spacecraft manufacturing sector continues to struggle. The production index declined 4.7 percent in October after increasing 7.2 percent in September. The sector remains down significantly, off 23.5 percent from last year.

Read the full article, which includes information about the U.S market and employment rates.

IPC International, Inc.

3000 Lakeside Drive, 105 N

Bannockburn, IL 60015

Tel.: + 1 (847) 615–7100

Website: www.ipc.org

{kind=link}