ZVEI, Central Association of the German electrical and electronics industry, sees the positive market trends already evident early last year continuing and gaining strength throughout 2004. That was the conclusion of a presentation recently in Munich, Germany.

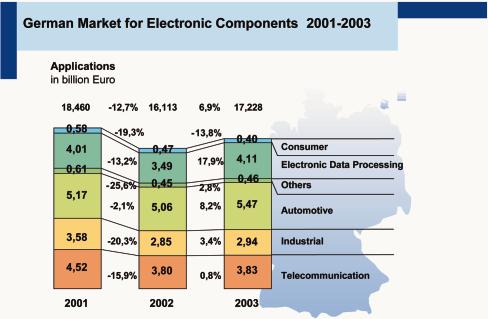

The overall German components market, largest in Europe, expanded last year by 7 %, reaching a total volume of €17.2bn. Of this, active components, including displays, CRTs and the like, gained 10 % to a volume of €11.6bn. Semiconductors, representing 90 % of active components, were pegged at €10.6bn. Processors and memory ICs showed the strongest growth, gaining 14.6 %. A major factor for this market rebound, says Peter Bauer of ZVEI, is the firming of average selling prices.

Germany’s strongest components consumer, with a market volume of €5.5bn, is the automotive industry. This represents a market share of 32 % and is still growing. The reason: even mid-range passenger cars get studded with complex systems for comfort, telematic, safety, motor controls, etc. Number two taking in electronic components is the datacom segment with a share of 24 %, overtaking telecom, which now holds 22.2 %. Industrial electronics follows with a share of 17 %. The consumer segment (5 %) continues to loose due to outward migration of production.

As a consequence, the automotive industry, Germany’s strength and pride, is contributing heavily to the current market recovery – for instance by consuming micro-mechanical sensors to the tune of €500m, which is an increase of 12 %. Passive components, though, remained in the doldrums: their unit numbers rose but with prices further declining. The same applies to mechanical components in general. The market volume of PCBs shrank by 0.6 % to a total €1.2bn, the level of 1995.

One caveat, when looking at global statistics: what looks like a decline in euro value can be a gain in Dollar terms, induced by fluctuating currency values. Measured in euro (one euro is about $ 1.30), the world market for components in 2003 shrank by 6.4 %, to a total volume of €271bn. In Dollar terms, however, this computes into a gain of 9.9 % or $300.5bn.

Globally, the shifting markets for electronic components due to the migration of manufacturing are even more pronounced. The winner in 2003, in Dollar terms, was East Asia, with a gain of 14.5 % ($108.9bn). However, converted into euro value, East Asia’s market volume shrank as well – by 2.5 %. Nevertheless, with a world market share of 36 %, East Asia is the largest market for components – and will be for the foreseeable future. Number two, again in euro terms, is America (22 %), followed by Japan (21 %) and Europe (19 %). Use the euro figures, ZVEI’s Peter Bauer cautions, only for intra-European calculations and comparisons. Electronic components are still sold and paid for in Dollars. WS

EPP EUROPE 408

Share:

{kind=link}